Master Negotiating A Jenks Commercial Lease: Expert Tips & Strategies

- Jul 27, 2025

- 16 min read

Updated: Jul 27, 2025

In Jenks you can’t win a negotiation at the table if you haven’t done the prep work first. The real victory in securing a great commercial lease happens long before you’re face-to-face with a landlord. It’s all about the strategic groundwork.

A winning negotiation is built on a simple foundation: knowing exactly what your business needs, having a solid grasp of the current market, and bringing in the right pros to fight for you. Getting this initial phase right sets the tone for everything that follows and gives you the power to land terms that actually help your business grow.

Laying the Groundwork for a Winning Negotiation

The biggest mistake I see Jenks business owners make? They start touring properties way too early. It's a classic error. They get starry-eyed over a space, and before they know it, they've signed on the dotted line, only to discover later it’s a terrible operational fit or they’re stuck with bad terms.

Trust me, this isn't a race. A successful negotiation is a calculated, deliberate process.

Define Your True Space Requirements

This goes way beyond just picking a square footage number out of the air. You have to get granular and think about how your business will actually live and breathe inside its new home. It’s about workflow, your team, and where you’re headed in the future.

Think through these critical points:

Workflow and Layout: How do your people work together? Do you need a big, open, collaborative buzz, or is it more about private offices and heads-down quiet zones? Sketch out your ideal flow to see what layout will make your team most effective.

Tech and Infrastructure: What are your non-negotiables? Be specific about internet speed, server room requirements, or any special electrical or plumbing you might need. A tech company and a retail shop have wildly different guts.

Your Growth Plan: Where will your business be in three, five, or even ten years? A great lease should give you room to grow, not box you in. This is where negotiating for a right of first refusal on an adjacent space can be a total game-changer down the road.

Accessibility and Brand Vibe: Your location needs to be easy for both employees and clients to get to. But it also has to feel right for your brand. A high-end law firm isn’t looking for the same building as a quirky startup coffee shop.

A well-defined needs analysis is your most powerful tool. It transforms your search from a vague "we need an office" to a specific "we need a 3,000 sq ft space with two private offices, a large open area, and fiber optic connectivity in a building with 24/7 access."

Do Your Market Homework

Once you know what you need, you have to figure out what’s a fair price. Walking into a negotiation without solid market data is like showing up to a gunfight with a knife. The landlord and their broker know the market inside and out—you need to arm yourself with that same intelligence.

Focus your research on key metrics right here in The Ten District. You’re looking for data on average rental rates per square foot for comparable properties. Pay close attention to vacancy rates; a high vacancy rate means you’ve got more leverage. Also, find out what kinds of concessions landlords are offering right now, like a few months of free rent or a tenant improvement allowance.

This intel gives you a realistic starting point for your first offer. Just like you’d map out every detail for a big community event, you need a data-driven plan for your lease. If you're organizing a local festival, our ultimate festival planning checklist offers a fantastic template for this kind of detailed prep.

Assemble Your A-Team

Trying to negotiate a commercial lease on your own is a huge risk. Landlords do this for a living. You need your own experts to level the playing field. Your team really comes down to two key players.

First, a commercial real estate broker who specializes in representing tenants. These pros have access to off-market listings, know the local scene cold, and have negotiated hundreds of deals. Best of all, their commission is almost always paid by the landlord, so their expertise doesn't come out of your pocket.

Just as critical is an experienced real estate attorney. Your broker handles the business side of things, but your attorney is there to pore over the dense legal language of the lease itself. They'll spot the hidden risks, vague clauses, and costly traps that could sink you years from now. By investing in this team, you’re building a protective wall around your business, ensuring you walk into that negotiation from a position of real strength.

Decoding Critical Lease Clauses and Terms

That lease document can feel like an intimidating wall of legal jargon. I get it. But you absolutely have to understand a few key clauses and rent structures before you sign anything. These terms will define your financial responsibilities and how you can operate for years. Getting them right from the start protects your bottom line and saves you from massive headaches down the road.

The language in that lease isn't just a formality; it's the rulebook for your entire tenancy. A single sentence can be the difference between a predictable monthly budget and surprise costs that cripple your cash flow. Let's break down the most critical pieces you'll come across when negotiating a commercial lease in The Ten District.

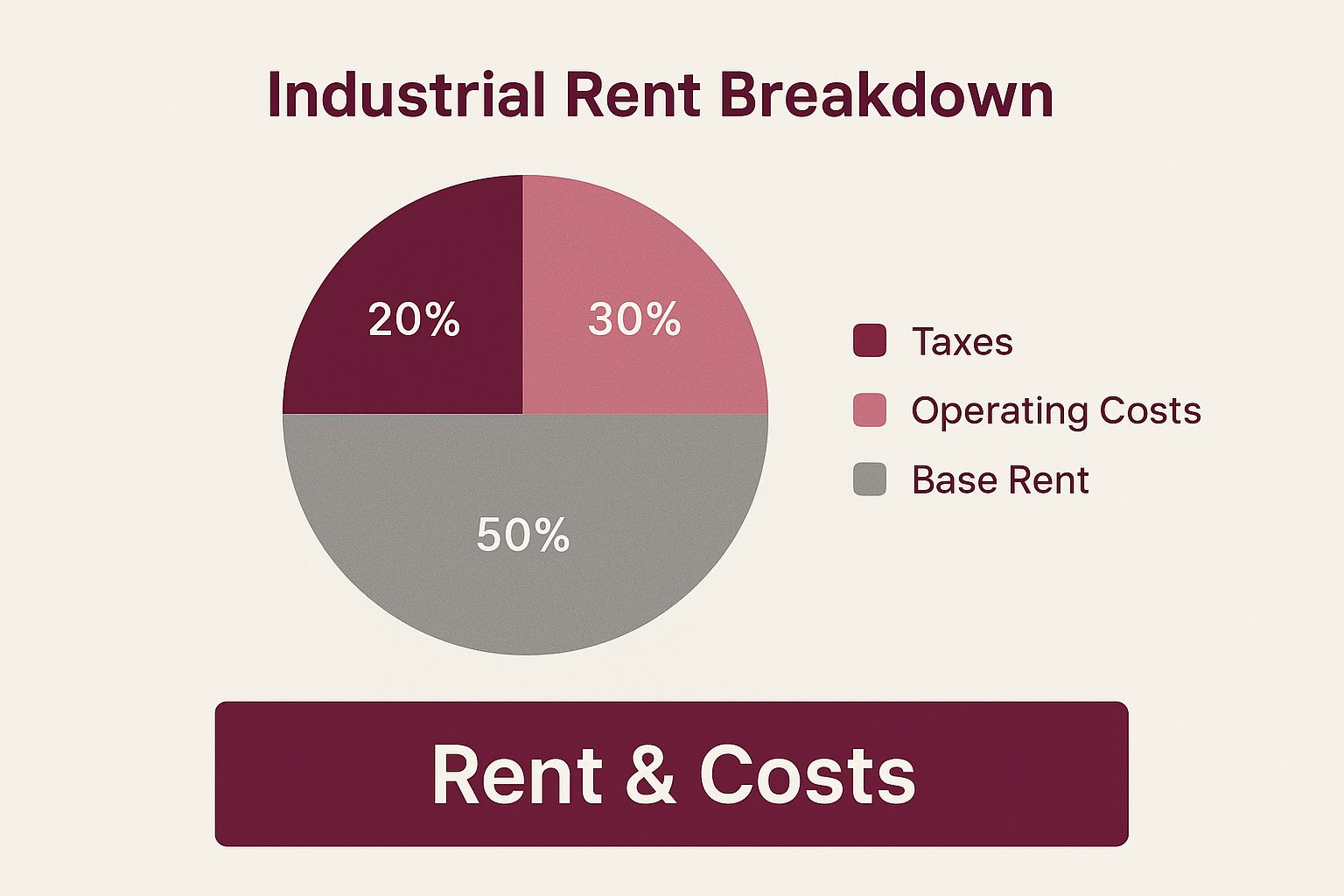

As you can see, your base rent is only one part of the puzzle. Those other operating costs can play a huge role in your total occupancy expense, so you need to know exactly what you're on the hook for.

Understanding Different Rent Structures

Your total monthly payment is shaped entirely by the lease structure. While the base rent is the number everyone focuses on, the type of lease determines who pays for all the other property expenses. A misunderstanding here can blow up your budget.

Landlords in The Ten District typically use one of three common rent structures. It's crucial to understand the nuances of each before you even get to the negotiating table.

Comparing Common Commercial Lease Structures | |||

|---|---|---|---|

Lease Type | Tenant Pays | Landlord Pays | Best For |

Triple Net (NNN) | Base Rent + Property Taxes + Building Insurance + Common Area Maintenance (CAM) | Structural repairs (roof, foundation) | Experienced tenants who want a lower base rent and can manage variable monthly costs. Very common for retail. |

Modified Gross | Base Rent + Some operating expenses (e.g., utilities, janitorial). Varies by lease. | Property taxes, insurance, CAM, and some operating expenses. | Businesses looking for a balance between the simplicity of a Gross lease and the lower base rent of an NNN lease. |

Full-Service Gross | One flat monthly rent payment. | All operating expenses, including taxes, insurance, CAM, and utilities. | Tenants who prioritize budget predictability and simplicity. Often found in large office buildings. |

The key takeaway? There's no single "best" lease type. It all depends on your business's financial model and your tolerance for fluctuating expenses.

Pro Tip: If you're looking at a Triple Net (NNN) lease, always ask for the property's expense history for the past 2-3 years. This is the only way to accurately forecast your potential costs and protect yourself from inheriting a building with sky-high maintenance fees.

Critical Clauses You Must Scrutinize

Beyond the rent, several other clauses hold immense power over your day-to-day operations. Don't skim these. Paying close attention here is a non-negotiable part of the process.

Lease Term And Renewal Options

The lease term is how long you're locked in, usually for 3, 5, or 10 years. Landlords almost always push for longer terms to secure their investment. As a tenant, a shorter term with renewal options gives you precious flexibility. A renewal option gives you the right to extend the lease, but make sure you negotiate the terms of that renewal—like rent increases—from day one.

Permitted Use And Exclusivity

The "permitted use" clause spells out exactly what business you can operate in the space. You need this to be broad enough to accommodate any future pivots. For instance, defining your use as just a "cafe" could be too restrictive if you decide later you want to sell retail merchandise.

An "exclusivity clause" is your competitive shield. It prevents the landlord from leasing another spot in the same building or shopping center to a direct competitor. For a specialty retail shop or a unique restaurant concept, this clause is priceless.

Alterations And Improvements

This clause defines your ability to change the space. Landlords want to protect their asset, so they will almost always require written consent for any significant changes. Try to negotiate for pre-approval on common alterations or at least a clear, straightforward process for getting projects green-lit. This is also where you'll hash out who pays for these changes through the Tenant Improvement (TI) allowance.

Managing the vendors and contractors for a build-out is a major project in itself. For some extra help on that front, our guide on vendor management best practices can be a lifesaver.

Maintenance And Repairs

Who fixes what? This needs to be spelled out with zero ambiguity. Typically, tenants are responsible for everything within their exclusive space, while the landlord handles the big structural things like the roof, foundation, and major building systems like HVAC. Vague language here is a recipe for expensive disputes. Get it in writing.

Proven Strategies for the Negotiation Table

You’ve done the legwork, sharpened your understanding of the fine print, and now it’s time to head to the negotiation table. This is where all that meticulous preparation really starts to pay off.

The goal here isn't to "win" in some old-school, adversarial sense. You're trying to forge a smart, sustainable agreement that sets your business up for success for years to come. Think of it less as a battle and more as the beginning of a long-term business relationship with your landlord. A good outcome depends on clear communication and a collaborative spirit.

Start with a Strong Letter of Intent

Before you get tangled in the dense, legally binding lease document, do what the seasoned pros do: start with a Letter of Intent (LOI).

Think of the LOI as a handshake agreement on paper. It’s a non-binding document that lays out all the major business terms of the deal before you sink a ton of time and money into legal reviews. It sets the framework for the formal lease and makes sure everyone is on the same page about what matters most.

Here’s what your LOI needs to cover:

Proposed Base Rent and Lease Structure: Get specific. Is it NNN, Modified Gross, or Full-Service Gross?

Lease Term and Renewal Options: Clearly state the initial term (e.g., five years) and any options to extend.

Tenant Improvement (TI) Allowance: Define exactly how much the landlord will kick in for your build-out.

Rent Abatement Period: If you’ve discussed any "rent-free" months, put it in writing here.

Key Clauses: Mention any non-negotiables, like exclusivity rights or permission to sublease.

Getting these core items down on paper first is a critical move. It smooths out the formal lease process and helps you sidestep major blow-ups later on.

Anchor Your Offers with Market Data

This is where your research becomes your superpower. Don't make offers based on what feels right—anchor every proposal with cold, hard data from The Ten District.

When you make a counteroffer, you should be able to reference comps, vacancy rates, and typical concessions you've already found. For example, you might say, "Our offer of $28 per square foot is based on the average for similar Class B spaces within a one-mile radius, which we’ve seen has a 12% vacancy rate."

This changes the entire dynamic. Your proposal is no longer just a request; it’s a well-reasoned business case. It proves to the landlord you’ve done your homework and you’re negotiating from a position of knowledge, not just hope.

A negotiation grounded in facts will always beat one based on feelings. Use market data to frame every offer and justify your requests for things like a few months of free rent or a bigger TI allowance. It makes it much harder for a landlord to just say no.

Keep the Big Picture in Mind

While you need to be firm, the best negotiations feel more like a collaboration than a fight. A "win-win" mindset builds a positive relationship from day one, and that goodwill can be invaluable when unexpected issues pop up down the road.

A landlord who sees you as a reasonable partner is far more likely to work with you. Building these local connections is key; you can even strengthen your network by joining one of the top local business networking groups in Jenks, OK to meet other professionals who can support your venture.

It's also interesting to note that negotiation styles vary. Here in North America, we tend to be direct, focusing on the numbers. In Europe, things can be more formal, while in many parts of Asia, building the relationship is the top priority. Understanding these nuances makes you a more effective negotiator, even right here in Jenks.

Ultimately, the goal is to show the landlord you respect their need for a secure investment while firmly advocating for what your business needs to thrive. Find that balance, and both of you can walk away feeling good about the deal.

Getting the Best Deal: Negotiating Financial Terms and Concessions

Here's where the real art of the deal comes into play. Honestly, negotiating a commercial lease isn’t just about the base rent you land on. The magic happens in the financial concessions you secure. These are the extra terms that can dramatically slash your total occupancy cost and give your business a healthy financial start right out of the gate.

Think of it this way: while the base rent is a fixed cost, things like a rent-free period or a hefty improvement allowance add serious value. They protect your cash flow when you need it most—during that chaotic and expensive move-in and setup phase.

Winning a Tenant Improvement Allowance

A Tenant Improvement (TI) allowance is cash the landlord kicks in to help you cover your build-out costs. This is probably one of the most critical concessions you can negotiate. It directly funds the process of turning a blank-slate space into one that actually reflects your brand and meets your operational needs.

Your mission is to lock in enough TI funding to handle the lion's share of your construction expenses. Landlords are usually more open to offering a bigger allowance if you're signing a longer lease—it’s a win-win. When you make your request, back it up with detailed quotes from contractors. This simple step shows the landlord you’ve done your homework and aren't just pulling a number out of thin air.

Be strategic about how you structure the payout of these funds:

Lump-Sum Payment: The landlord gives you the full allowance after you've finished the work and provided paid invoices. This method works, but you'll need significant cash on hand to front the costs.

Direct Payment to Contractors: This is a common and often better approach. The landlord pays your contractors directly as they complete milestones, which takes a huge out-of-pocket burden off your shoulders.

Rent Credit: The allowance gets applied as a credit toward your future rent payments.

A strong TI allowance negotiation can be the difference between a smooth launch and a project that’s drowning in budget overruns. Don’t be shy about asking for what you need, especially if you’re a desirable tenant committing to a long-term lease.

Negotiate for a Rent-Free Period

A rent-free period, or what's sometimes called rent abatement, is just what it sounds like: a few months where you get to occupy the space without writing a rent check. This is an incredibly valuable concession. It gives you some breathing room financially during your build-out and grand opening.

I’ve seen clients use this time to cover all sorts of startup costs, from moving expenses to the marketing blitz for their launch. The length of the rent-free period is highly negotiable and often hinges on your lease term and the current market. If vacancy rates are high, landlords are much more motivated to offer several months of free rent to lock in a quality tenant.

Let's look at recent history. The COVID-19 pandemic completely shook up commercial real estate. In the third quarter of 2020 alone, U.S. office occupancy dropped by a historic 28.9 million square feet. This pushed vacancy rates up to 16%, which in turn forced over 70% of landlords to pause or renegotiate leases with new terms, including rent abatement. It created a more collaborative environment where concessions became the norm to avoid empty storefronts.

Cap Your Common Area Maintenance Charges

If you're looking at a Triple Net (NNN) lease, you're on the hook for Common Area Maintenance (CAM) charges. These costs can cover everything from landscaping and snow removal to parking lot repairs and management fees. The problem is, without a cap, they can become a runaway train of unpredictable expenses.

You absolutely need to insist on negotiating a hard cap on CAM increases. A standard cap will limit the annual increase to a fixed percentage, like 3-5%, or tie it to the Consumer Price Index (CPI). This gives you predictability and ensures your budget won't get torpedoed by a landlord’s surprise project.

Securing these financial wins takes a bit of strategy. Landlords are running a business, of course, but they also want to fill their spaces and create a thriving commercial environment. Initiatives like the [Jenks Main Street Project](https://www.thetendistrict.com/jenks/jenks-main-street-project-an-update-from-councilor-john-brown) demonstrate a real commitment to building vibrant districts, and property owners in these areas are often eager to attract strong, long-term tenants. Use your position as a valuable new business to secure the terms that will set you up for success.

Building in an Exit Strategy and Future Flexibility

Let's be realistic: your business isn't static. It’s going to grow, pivot, and evolve. Your commercial lease needs to be built to handle that journey right alongside you. One of the most critical things to think about when you're negotiating a lease is how you're going to get out of it if you need to.

Thinking about your exit strategy on day one isn't being pessimistic; it's just smart business. This is especially true for startups and small businesses where the future has a lot more question marks than answers. These clauses aren't just a nice-to-have—they're a vital safety net that can protect you from getting trapped in a space that no longer fits.

Navigating Assignment and Subletting Clauses

Two of the most powerful tools for future-proofing your lease are the assignment and subletting clauses. An assignment lets you hand off your entire lease to another business, while subletting allows you to rent out just a portion of your space.

You'll often see landlords try to slip in language that gives them "sole discretion" to approve or deny these requests. That's a huge red flag. Your goal is to get that changed to require the landlord to be "reasonable" in their decision. This simple word change stops them from arbitrarily blocking a perfectly good replacement tenant.

Imagine your business explodes and you need to double your space. A reasonable assignment clause means you can find a qualified new tenant to take over your current lease, freeing you up to move without paying rent on two locations. Without it, you’re stuck.

The Power of an Early Termination Right

An early termination right, sometimes called a break clause, is your planned escape hatch. It’s a pre-negotiated option to end the lease before its official expiration date, usually after a certain amount of time has passed and for a set fee. Landlords aren't always thrilled to grant these, but they become much more negotiable if you’re signing a longer-term lease.

A typical early termination right might look something like this:

You get a one-time option to terminate after the 36th month of the lease.

You must give 6 months' written notice.

You have to pay a termination fee equal to 4 months' rent.

Yes, that fee can feel steep, but it’s a drop in the bucket compared to paying rent for years on a space you can't even use.

In the world of commercial leasing, small businesses often start at a disadvantage. There's a natural information imbalance; landlords and their brokers live in this market daily, while tenants may only engage once every few years. This can lead to less-than-ideal terms if you aren't prepared. To counter this, it's crucial to employ win-win strategies that thoughtfully address key areas like assignment and subletting. Gaining a deep understanding of these clauses is a powerful way to level the playing field.

It's just like planning for a big event—you anticipate potential issues to avoid disaster. Thinking through **crowd management strategies for events in Jenks** shows how foresight prevents logistical nightmares, and that lesson applies directly to leasing. By securing flexible terms now, you're making sure your lease is a tool for your success, not a roadblock.

Common Questions About Commercial Lease Negotiations

Stepping into the world of commercial real estate can feel like a lot, and it's totally normal to have questions. Negotiating a commercial lease is a high-stakes game where one small oversight can echo through your finances for years.

The best way to feel confident is to get clear, straight-up answers to the things that might be worrying you. So, let’s get into some of the most common questions we hear from business owners before they even think about signing on the dotted line.

Do I Really Need a Broker and a Lawyer?

Yes. Without a doubt. Trying to navigate this process on your own is a huge gamble that you really don't want to take. Think of a commercial broker and a real estate attorney as your essential one-two punch—each playing a critical, but very different, role.

Your broker is your boots-on-the-ground market expert. They know what spaces are really renting for, what kind of perks and concessions landlords are giving out right now, and they often have the inside track on properties that aren't even publicly listed. Their job is to find you the right spot and handle the business end of the deal.

Your attorney, on the other hand, is your legal guardian angel. They're the ones who will pour over that dense lease agreement—which, by the way, is almost always written to heavily favor the landlord. They’re trained to sniff out hidden risks, fuzzy language, and clauses that could trap you later. The landlord has their team of experts; walking in without yours is like showing up to a gunfight with a knife.

What Are Some Major Red Flags in a Lease?

There are a few clauses that should make you sit up and pay very close attention. Spotting these red flags is a massive part of protecting your business from a future headache.

Be on high alert for these troublemakers:

An Uncapped Operating Expense Clause: This one is a big deal, especially in a Triple Net (NNN) lease. Without a cap, you’re basically giving the landlord a blank check to pass along property costs. It makes your budget a complete guessing game.

A Super Restrictive "Assignment and Subletting" Clause: Things change. Businesses grow, and sometimes they need to pivot. If this clause gives the landlord "sole discretion" to say no if you need to assign or sublet your lease, you could be stuck paying for a space you can't even use.

A "Relocation" Clause: This is a sneaky one. It gives the landlord the power to move your business to another spot in the building, which is almost always a less desirable one. Talk about a nightmare for your operations and your customers.

If a landlord digs in their heels and won't budge on these fundamental points, it can be a serious warning sign. It often signals a difficult and inflexible partnership ahead. Remember, sometimes the best deal is the one you walk away from.

How Long Does the Negotiation Process Usually Take?

You have to be patient here. Rushing through a commercial lease negotiation is the fastest way to get stuck with bad terms. Realistically, the whole process—from starting your search to holding a signed lease—can easily take one to four months. Sometimes even longer.

Let’s break that down:

Finding the Right Property: A few weeks to a month.

Negotiating the Letter of Intent (LOI): This usually takes one to three weeks of back-and-forth.

Lease Document Review: This is where things can really drag out. The lawyers for both sides will trade revisions, and this stage alone can last three to six weeks.

A good rule of thumb? Start your search at least six to nine months before you absolutely need to be in the new space. That buffer gives you breathing room for a proper negotiation, a thorough legal review, and any construction you have planned, all without feeling the pressure to sign a deal you'll regret.

Are you ready to find the perfect space for your business in the heart of Jenks? Explore the opportunities waiting for you at The Ten District, where community and commerce come together. Visit us at https://www.thetendistrict.com to learn more.

Comments