How to Evaluate Commercial Property for Maximum ROI

- Dec 29, 2025

- 17 min read

Before you even think about signing a lease or making an offer on a commercial property, you need a game plan. It’s too easy to get caught up in the potential of a beautiful storefront or a great-sounding deal without digging into what really matters.

Getting this right means looking past the listing price to uncover the property’s true potential—and its hidden problems. This is about making a smart business decision based on hard facts, not just a gut feeling.

Your Framework for Smart Property Decisions

Whether you're an entrepreneur eyeing a retail spot in a growing downtown like Jenks, or an investor sizing up a multi-tenant building, the core process is the same. You need a repeatable framework that takes the mystery out of the evaluation.

This isn’t just about kicking the tires. It’s about building a complete picture of the asset, blending the hard numbers with the on-the-ground reality.

The Three Pillars of Evaluation

A rock-solid property evaluation comes down to three key areas. Think of them as different lenses for looking at the same opportunity. If you skip one, you’re flying blind.

Financial Analysis: This is where you get real about the numbers. It’s all about digging into the income statements, calculating critical metrics like Net Operating Income (NOI) and Cap Rate, and projecting future performance to see if the property can actually make money.

Physical & Legal Due Diligence: Here, you’re focused on the tangible and regulatory stuff. This covers everything from building inspections and environmental checks to confirming zoning laws and combing through the title history. You're looking for any physical defects or legal headaches that could derail your plans.

Market & Location Analysis: A property doesn’t exist in a vacuum. Its success is completely tied to its surroundings. This means studying local demographics, economic trends, who your competitors are, and how accessible the location is. Will this spot support your goals for the long haul?

By methodically working through these three pillars, you stop looking at a property and start conducting a strategic business analysis. You're building a story that either backs up the investment or waves the red flags telling you to walk away.

This approach helps you find the real opportunities and spot deal-breakers early on. Local market context is everything. Understanding the specific dynamics of a place undergoing a revival, for example, requires a much sharper focus. You can learn more about that in our guide to small town revitalization strategies.

Ultimately, using a solid framework like this ensures your final decision is the right one for your goals.

Getting to the Bottom Line: Decoding a Property’s Financials

When you’re looking at commercial property, the real story isn't just about the fresh paint or curb appeal—it’s hidden in the numbers. Financial analysis is the bedrock of any smart investment. It’s what separates a true income-producer from a money pit in disguise. This is where you move past feelings and let the cold, hard data do the talking.

The first step is getting your head around the core metrics. These aren't just buzzwords; they’re the tools you’ll use to dissect a property’s health and stack it up against other opportunities. Getting this right is non-negotiable for any serious buyer or tenant.

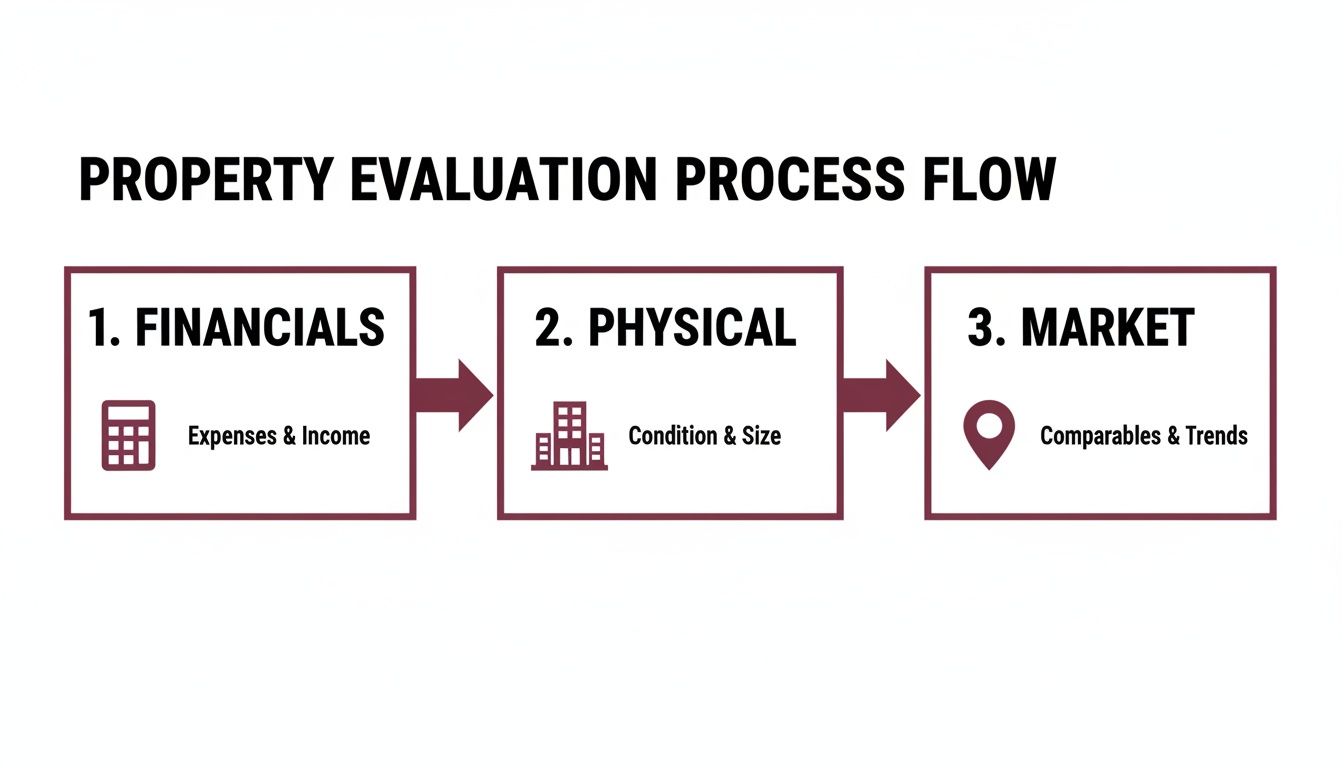

Think of it as a three-part process: financials first, then the physical property, and finally the market itself.

This simple flow shows why everything starts with a solid financial foundation. If the numbers don't work, nothing else matters.

Net Operating Income (NOI): The True Measure of Profit

If there’s one number you absolutely must understand, it’s the Net Operating Income (NOI). Simply put, NOI is the property's total income minus all its necessary operating expenses. It’s a pure look at how much profit the building itself generates, before things like mortgages or income taxes enter the picture.

Here’s how you get there. Start with the Gross Potential Income (GPI), which is what you’d make if the property was 100% occupied. Then, you subtract what you’ll likely lose to vacancies and unpaid rent, and add any extra income (like parking fees) to find the Effective Gross Income (EGI).

From that EGI, you deduct your operating expenses:

Property taxes

Insurance

Maintenance and day-to-day repairs

Utilities

Property management fees

What’s left is your NOI. This is the figure that tells you what the asset itself earns, completely separate from your personal financing situation.

Cap Rate: Your Go-To for Quick Comparisons

With the NOI in hand, you can figure out the Capitalization Rate (Cap Rate). The cap rate is an incredibly useful metric for quickly comparing the potential returns of different properties. It’s the property’s unleveraged rate of return.

The formula couldn’t be simpler: Cap Rate = Net Operating Income / Current Market Value (or Purchase Price). A higher cap rate often points to a higher potential return, but it can also signal higher risk.

When it comes to commercial real estate, the Income Approach is king. In fact, between 2010 and 2020, this method was used in over 75% of U.S. appraisals for office, retail, and multifamily properties. The whole thing boils down to Value = NOI / Cap Rate. In 2020, retail cap rates in major U.S. markets were hovering around 6.5%, which means a property with a $500,000 NOI was likely valued around $7.7 million.

Let’s bring it local. Say a small retail spot in Jenks is listed for $1 million and its NOI is $70,000. The cap rate is 7% ($70,000 / $1,000,000). If a similar building down the street has a 6% cap rate, that first property is probably offering a better bang for your buck, at least on paper.

Cash-on-Cash Return: What’s Actually Hitting Your Pocket?

While cap rate is great for a quick look, the Cash-on-Cash Return tells you the real-world return on the actual money you pulled out of your pocket. This is crucial because almost nobody buys property with all cash; financing is part of the game.

The calculation is: Cash-on-Cash Return = Annual Pre-Tax Cash Flow / Total Cash Invested.

Let's unpack that. Your annual cash flow is your NOI minus your yearly mortgage payments. The total cash you invested is your down payment plus any closing costs and upfront repair expenses. This metric shows you exactly how hard your invested dollars are working for you.

To help keep these key metrics straight, here's a quick cheat sheet.

Key Financial Metrics at a Glance

Metric | Formula | What It Tells You |

|---|---|---|

NOI | Gross Income - Operating Expenses | The property's raw profitability, independent of financing. |

Cap Rate | NOI / Property Value | The unleveraged rate of return; great for comparing different deals. |

Cash-on-Cash Return | Pre-Tax Cash Flow / Total Cash Invested | Your actual return on the money you put into the deal. |

This table is a handy reference, but remember, each metric tells only part of the story. You need to look at them together to get the full picture.

Pro Forma: Your Financial Crystal Ball

Finally, we have the pro forma statement. Think of it as a financial forecast for the property. It’s an educated guess, sure, but it's an absolutely essential one. You’ll take the seller's current financials as your starting point, then adjust everything based on your own research, experience, and plans for the property.

Are you planning to raise rents? Do you see a way to cut down on utility costs? Or do you think vacancy rates in the Jenks market might tick up? A good pro forma will map out a five- or ten-year projection of income, expenses, and cash flow, giving you a much clearer picture of the investment’s long-term potential.

Getting these projections right is what gives you leverage at the negotiating table. For more on that, check out our guide to master negotiating a Jenks commercial lease.

Getting Your Hands Dirty: A Deep Dive into Physical and Legal Due Diligence

Okay, the spreadsheet looks promising. The numbers pencil out, and you're starting to feel good about this deal. Now comes the real work—the part where you move from theory to reality. This is the due diligence phase, and it’s all about getting your hands dirty to uncover the physical and legal truths that a pro forma can't tell you.

Think of this as the investigation stage. You're looking behind the curtain to protect your investment from the kind of expensive surprises that can sink a deal after it's too late. Trust me, cutting corners here is one of the biggest mistakes a buyer can make.

Kicking the Tires the Right Way

A property's physical condition is a massive variable in its true long-term cost. A low purchase price means nothing if you're suddenly facing a $50,000 roof replacement or a failing HVAC system in your first year. This is why professional inspections are absolutely non-negotiable.

Don't just hire one general inspector and call it a day. Commercial properties are complex, with systems that demand a specialist's eye.

Your inspection team should include experts for:

Structural and Foundation: Someone who can assess the building's core integrity and spot signs of settling or stress.

Roofing: A commercial roofer is essential. They'll give you a real estimate of its remaining lifespan and potential repair costs.

HVAC Systems: These units are major capital expenses. You need to know their exact condition.

Plumbing and Electrical: Are the systems up to code? Can they handle your business's demands?

ADA Compliance: Verifying the property meets the accessibility requirements of the Americans with Disabilities Act is crucial to avoid future headaches.

Every report you get is more than just information—it's leverage. Use these findings to negotiate repairs or a price adjustment with the seller.

Uncovering Hidden Environmental Risks

What you see is one thing. What might be lurking in the soil or groundwater is another entirely. This is where an Environmental Site Assessment (ESA) becomes critical. An ESA is a formal report that flags potential or existing environmental contamination liabilities.

The standard starting point is a Phase I ESA. This involves digging into historical records, inspecting the site, and conducting interviews to see if there's a contamination risk. If any red flags pop up—say, the property was once a gas station or a dry cleaner—you'll likely need a Phase II ESA, which involves actual soil and water testing.

Ignoring environmental due diligence is a huge gamble. Cleanup costs can easily soar into the hundreds of thousands of dollars, and as the new owner, that liability could land squarely on your shoulders.

Navigating the Legal Labyrinth

Just as crucial as the building itself is its legal standing. You need absolute certainty that you can legally run your business the way you envision. This part of your diligence zeroes in on zoning, titles, and any existing agreements.

Zoning and Land Use Verification

Zoning laws dictate exactly how a property can be used. A space might look perfect for your new restaurant, but that doesn't mean the city agrees. You have to verify that the property’s zoning designation allows for your specific business operations.

For example, a property could be zoned for general retail but have restrictions against serving alcohol or staying open past a certain hour. The devil is always in the details. To get a handle on how these rules work locally, check out our comprehensive guide to Oklahoma zoning codes. It’s essential for ensuring your plans for a spot in The Ten District or anywhere in Jenks align with city ordinances.

Title Search and Survey Review

You need a clean title, period. A professional title search confirms the seller has the legal right to sell and, more importantly, uncovers any liens, easements, or other restrictions tied to the property. An old mechanic's lien or an undisclosed utility easement can create major legal and financial problems down the line.

At the same time, get your hands on a recent property survey. A survey confirms the property's boundaries, identifies any encroachments (like a neighbor’s fence on your land), and verifies access points. It ensures you know exactly what you’re buying.

Scrutinizing Tenant Leases

If you're buying a property that's already occupied, the existing leases are either a major asset or a potential liability. You have to review every single lease agreement in excruciating detail. Pay close attention to:

Lease Terms: How much time is left on the leases? Are there renewal options?

Rent Rolls: Does the rent being collected match what's stated in the leases?

Landlord Obligations: What maintenance and repair responsibilities are you inheriting from the previous owner?

These documents define your future income. Understanding them is fundamental to confirming the financial projections you ran earlier. A building full of strong leases with creditworthy tenants adds immense value; a portfolio of weak or problematic ones can be a significant drain.

Gauging the True Potential of a Location

You can find the most beautiful building in the world, but if it's in a lousy location, you've got a recipe for failure. Once the numbers make sense and the building itself passes muster, your focus has to shift outward. The success of any commercial property is tied directly to its surroundings, which is why a deep dive into the local market is a non-negotiable part of your evaluation.

This isn't just about glancing at a map. It's about getting to know the living, breathing ecosystem your business is about to join.

You need to peel back the layers of the community to see if your venture can actually thrive here. It’s about making sure the location has the staying power and the right customer base for long-term growth, not just surviving the first year.

The Human Element: Who Are Your Customers?

First things first: you need to understand the people. Who lives here? Who works and shops in this area? Your local city planning department or economic development agency is a goldmine for this stuff. They can give you detailed reports on population density, average household income, age ranges, and local spending habits.

These numbers tell a story. For instance, an area packed with young families is a great signal for a kids' boutique or a casual restaurant. An area dense with office buildings? That's a built-in lunch and coffee crowd just waiting for you.

But data only gets you so far. You have to get out there and feel the pulse of the neighborhood. Go hang out at the property on different days, at different times.

Is the area buzzing with foot traffic on a Tuesday afternoon, or is it a ghost town until Saturday?

How easy is it for people to get to you? Look at parking, public transit, and how walkable the streets are.

What’s the drive-time traffic like? Being highly visible from a busy road can be a game-changer.

This on-the-ground intel is pure gold. It turns spreadsheets and charts into a real-world picture of how customers will actually find and interact with your business. You'll spot opportunities—and potential headaches—that the numbers alone will never show you.

Sizing Up the Neighborhood: Competition and Co-Tenancy

No business exists in a vacuum. You've got to get a handle on the local competition. Who are your direct competitors? What are they doing right, and where are their weaknesses? The last thing you want is to enter a market that’s already oversaturated. Look for the gaps.

Just as critical is the idea of co-tenancy—basically, who your neighbors are. The right ones can create an incredible synergy that drives a ton of business your way. Think about a high-end salon opening next to a popular women's clothing store. They feed off each other.

On the flip side, a bad tenant mix can drag you down. Setting up shop next to a struggling or mismatched business can hurt how people see your brand. When you're looking at a spot in a growing area like The Ten District, the planned tenant mix is a huge clue about the area's future vibe and target audience.

Looking Ahead: What's on the Horizon?

A snapshot of today isn't enough. You have to be a bit of a fortune teller. What’s coming next for this area? Researching future development plans is absolutely essential for understanding the long-term trajectory of your investment.

Get in touch with the local planning and zoning department. You'll want to ask about:

Upcoming public projects: Are new roads, parks, or transit lines in the works? These can make a location way more attractive and accessible.

Major private developments: Is a big residential complex or corporate headquarters being built nearby? That could mean a flood of new customers.

Zoning changes: Are there any proposals that could change the whole character of the neighborhood, for better or for worse?

Economic trends are a huge piece of the puzzle, too. The recent opening of the Tulsa Premium Outlets is a perfect example of a development that injects new life and a major economic boost into the Jenks area. These kinds of projects can lift the entire market, driving up property values and foot traffic.

To really get a grip on the physical layout and boundaries that these developments impact, it's wise to consult a guide on how to survey land. This foundational step helps you see exactly how new projects will fit in with existing property lines.

Determining Fair Market Value Before You Offer

You’ve run the numbers, walked the property, and dug into the local market. Now it’s time to answer the million-dollar question: what’s this place actually worth? Figuring out the fair market value is where all your hard work comes together, transforming stacks of research into a solid, defensible offer.

This isn't about pulling a number out of thin air. It’s about using proven valuation methods to build a logical case for a specific price. Get these down, and you'll have the confidence to spot an overpriced listing from a mile away and the data to back up your own number when you slide that offer across the table.

The Sales Comparison Approach Using Comps

The most straightforward way to value a property is the Sales Comparison Approach. The idea is simple: a property is worth whatever similar properties have recently sold for. We call these "comps," and finding truly comparable ones is the key to getting this right.

You can't just compare any two retail buildings and call it a day. A real comp needs to be similar in a few key ways:

Location: You want properties in the same submarket. Think downtown Jenks, not just anywhere in Tulsa County.

Size: Look for buildings within a 15-20% size range of your target property.

Age and Condition: A shiny new build isn't a fair comparison for a 30-year-old property that needs a new roof.

Property Type and Use: A single-tenant restaurant operates very differently from a multi-tenant retail strip. The value drivers just aren't the same.

Once you’ve found three to five solid comps, the real analysis begins. You have to adjust their sale prices to account for the differences. Did a comp have a brand-new HVAC system? You'll need to adjust its price downward to normalize it against your target property. Does your property have better road frontage? You might adjust the comp's price upward. This process gives you a realistic, market-supported value range. A deep dive into the local market can be incredibly helpful here; our guide to Jenks real estate provides valuable context for finding relevant comps.

The Income Approach Revisited

We already talked about the financial metrics that drive the Income Approach, especially the critical relationship between Net Operating Income (NOI) and the Cap Rate. For most commercial investments, this is the most important valuation method because it values a property based on its ability to generate cash flow.

The formula is straightforward: Market Value = Net Operating Income / Capitalization Rate. Your job is to make sure the NOI you're using is verified and realistic, not just the seller's pie-in-the-sky projection. You also need to apply a cap rate that accurately reflects the current market conditions for that property type and location.

When to Use the Cost Approach

The third method, the Cost Approach, is more of a specialist’s tool, but it's essential in certain situations. This approach figures out a property's value by calculating what it would cost to build an identical one from the ground up today.

It's most useful for unique properties that don't have good comps—think a church, a school, or a custom-built public venue. For a landmark spot in The Ten District with unique architecture reflecting Oklahoma heritage, the Cost Approach provides a solid baseline. The method works by adding the land value (found by looking at recent sales of vacant lots) to the replacement cost of the building, then subtracting depreciation. For context, in 2025, U.S. commercial construction costs are averaging $200-350 PSF for new retail. A 15,000 sq ft property might cost $4.5 million to build new, but you’d then depreciate that number by 20-30% if the existing structure is 20 years old.

Synthesizing the Data to Craft Your Offer

It's rare for all three valuation methods to spit out the exact same number. The real skill is in reconciling the different figures to arrive at a final conclusion of value. For an income-producing retail strip, you’ll lean heavily on the Income Approach. For a vacant building you plan to occupy yourself, the Sales Comparison Approach will likely be your primary guide.

Once you have your number, you're ready to make an offer. But remember, an offer is more than just a price—it includes terms that can save you a lot of headaches down the road.

Be sure to negotiate terms like:

Due Diligence Period: Give yourself enough time (30-90 days) to complete all your inspections without being rushed.

Financing Contingency: This is a crucial clause that lets you walk away if you can't secure a loan.

Seller Concessions: Use what you find during inspections to negotiate credits for necessary repairs.

Before you finalize anything, it’s always smart to explore various top real estate valuation methods to be sure you're arriving at a fair market price. Having a firm grasp on your property’s value, backed by solid data, is your greatest source of leverage in any negotiation. It lets you move forward with conviction, knowing your offer is grounded in a thorough and professional evaluation.

Got Questions? Let's Talk Real-World Scenarios

Even when you have a solid plan for evaluating a commercial property, the process always throws a few curveballs. Every deal is different, and specific questions are bound to pop up.

Whether you're a seasoned pro, a small business owner finally buying your own building, or a retailer trying to find that perfect spot to lease, getting the right answers is everything. It's the difference between a smooth, profitable deal and a costly headache. Let's break down some of the most common questions I hear.

How Long Do I Really Need for Due Diligence?

This is one of the first and most critical questions in any deal. A typical due diligence period can run anywhere from 30 to 90 days, but remember, this is always negotiable. The right timeline really depends on the property itself.

If you're looking at something straightforward—say, a small, single-tenant retail building with clean financials—you might be able to get everything done in 30 days. That usually gives you enough time for physical inspections, a basic environmental review, and a title search.

But for a more complicated property, like a multi-tenant office building or a shopping center with a dozen different leases, you've got to give yourself more runway. For those, 60 to 90 days is much more realistic. You'll need that extra time to dig into every single lease, conduct a serious financial audit, and line up more specialized inspections.

My advice? Always ask for more time than you think you'll need. It's far better to have a cushion than to be scrambling last-minute to ask the seller for an extension. That can really weaken your position at the negotiating table.

What are the Biggest Mistakes People Make?

Knowing what not to do is just as important as having a good checklist. Over the years, I've seen a few common mistakes trip up even savvy buyers.

Here are the big ones to watch out for:

Underestimating Expenses: This is the #1 pitfall, hands down. A seller might hand you financials that conveniently downplay operating costs to inflate the Net Operating Income (NOI). Don't trust it. Build your own budget from the ground up using real, verified numbers.

Skimping on Inspections: It's so tempting to save a couple of grand by skipping the specialized roof or HVAC inspection. This is a classic "penny-wise, pound-foolish" move. That "savings" vanishes pretty quickly when you're hit with a $50,000 bill for a new roof a year after closing.

Ignoring Local Zoning: Never, ever assume your business concept is a permitted use for a property. You have to go straight to the city and verify the zoning. The nightmare scenario is closing on your dream spot only to find out your business is completely prohibited there.

Believing the Pro Forma: Think of a seller's pro forma as a marketing brochure, not a crystal ball. It’s their best-case-scenario forecast. Always run your own numbers based on the actual rent roll and historical expenses to build a financial model you can truly stand behind.

What Should a Tenant Focus On?

If you're a tenant, your evaluation is less about ownership and more about operations, but it's just as critical. You’re not just renting space; you’re choosing a partner in your business's success.

Here's what you need to zero in on:

Location, Location, Accessibility: Is this spot right for your business? Get out there and analyze the foot traffic, street visibility, and customer parking. Can your target audience find you and get to you easily? For a retail shop in a place like downtown Jenks, this is everything.

The Lease Itself: This is your bible for the next 3, 5, or 10 years. You need to understand every word. Pay special attention to the lease type (NNN, Gross, etc.), how much the rent goes up each year, and exactly who pays for what—maintenance, repairs, and big-ticket capital improvements.

The Landlord's Reputation: Do some digging. Is the landlord known for being responsive and keeping their properties in top shape? Or do they have a reputation for being impossible to reach when the A/C goes out? A bad landlord can make your day-to-day operations a struggle.

Your Neighbors (The Co-Tenancy Clause): Look at the businesses around you. Are they strong, complementary brands that will bring in more customers? A great tenant mix can be a rising tide that lifts all boats. A center full of struggling stores can drag you down with it.

Here at The Ten District, we know that a thriving business starts with the right foundation. Our curated district in the heart of Jenks is creating a unique environment where community and commerce grow together. It's the perfect place to build your next venture.

Ready to see for yourself? Discover your ideal space in The Ten District.

Comments