Gateway Mortgage Jenks: Your Trusted Home Loan Guide

- Aug 30, 2025

- 14 min read

So, you're thinking about buying a home in Jenks. It's an exciting thought, and finding the right local lender can make all the difference in turning that thought into reality. For a lot of folks around here, that lender is Gateway Mortgage. They're not just some faceless bank; they're a cornerstone of the community, and that local know-how is exactly what you need to navigate the process and land your dream home.

Let’s walk through what it really looks like to get your home loan with them.

Your Home Loan Journey with Gateway Mortgage in Jenks

Choosing a mortgage lender can feel like a huge task, but picking one with deep roots right here in Jenks gives you a serious leg up. Gateway isn't just a national name with a local office; it’s a Jenks-based company that genuinely gets the local real estate market.

That connection pays off in real ways for homebuyers. Their loan officers know the neighborhoods inside and out. They understand the property value trends from The Arkansas River to South Jenks and have solid relationships with local real estate agents and title companies. This kind of insider knowledge is gold, especially when the market gets competitive. It just makes the whole process—from application to closing day—run a lot smoother.

A Legacy of Local Commitment

Gateway's story is a Jenks story. It all started back in 2000 when J. Kevin Stitt launched the company with little more than a vision. From those humble beginnings, Gateway Mortgage grew into one of the biggest mortgage operations in the country, with its heart still right here in Jenks.

After becoming a Federal Housing Administration lender in 2002, they began expanding nationally. Then, in 2019, a merger with a community bank that had been around for a century broadened their services even further. It created this powerful mix of comprehensive mortgage options and real, community-focused banking.

Key Takeaway: Choosing Gateway Mortgage means you're not just another loan application. You're working with a team that's personally invested in seeing the Jenks community thrive.

Why a Jenks-Based Lender Matters

When you work with Gateway, you’re not just getting a loan. You're getting a partner who understands what makes this place special, and that’s a huge asset when you’re making one of the biggest financial decisions of your life.

If you're new to the area or just want to learn more about what makes this town tick, our guide to life in Jenks, Oklahoma is a great place to start.

Here's a snapshot of what to expect:

Personalized Guidance: You'll sit down with a loan officer who lives and works right here, offering advice that’s actually relevant to your goals.

Market Insight: They can give you the real-time scoop on Jenks-specific trends that could shape your homebuying strategy.

Streamlined Communication: Being local means they can pick up the phone and get things done quickly with the other local players in your transaction.

To give you a clearer picture, here’s a quick breakdown of what makes Gateway a strong choice for anyone looking to buy in Jenks.

Gateway Mortgage Jenks At a Glance

Feature | Description | Why It Matters for Jenks Homebuyers |

|---|---|---|

Founding Year | 2000, right here in Jenks, Oklahoma. | Decades of experience navigating the specific nuances of the Jenks and greater Tulsa real estate markets. |

Local Headquarters | A major employer and financial institution based in Jenks. | Deep community ties and a vested interest in the area's economic health, which benefits local borrowers. |

Key Milestone | Became a Federal Housing Administration (FHA) lender in 2002. | This opened up more accessible loan options, like FHA loans, which are popular with first-time homebuyers in the area. |

Major Expansion | Merged with a century-old community bank in 2019. | Gained the ability to offer a full suite of banking services alongside their mortgage expertise. One-stop shopping. |

Loan Officer Expertise | Loan officers are local residents with established networks. | They know the real estate agents, appraisers, and title companies, ensuring a more cohesive and efficient closing process. |

Ultimately, having a lender who understands the local landscape can be the difference between a stressful process and a smooth path to homeownership.

Getting Ready for a Successful Mortgage Application

Before you even step into Gateway Mortgage Jenks, a little prep work can make all the difference. Think of it as your pre-game strategy. Getting organized now ensures the entire process is smoother and sets you up for success.

This isn't just about shuffling papers. It’s about understanding the financial story you're presenting to a lender and making sure it's a compelling one. When you walk in prepared, it sends a clear signal that you’re a serious, organized, and reliable borrower.

Gather Your Core Financial Documents

The first thing I always tell people is to create a "mortgage folder," whether it's a physical file or a digital one on your computer. Lenders need to verify everything—your income, your assets, your financial history—so having it all in one spot will save you a ton of time and headaches later.

Here’s a quick list of what you'll need to pull together:

Proof of Income: You'll want your last 30 days of pay stubs and your W-2s from the last two years. If you're self-employed, the ask is a bit different: two years of tax returns and a recent profit-and-loss statement.

Asset Information: Grab your two most recent bank statements for every checking and savings account you have. Don't forget statements for any retirement or investment accounts, too.

Personal Identification: Make sure you have your driver's license (or another government-issued ID) and your Social Security card handy.

This isn't about guesswork; lenders are legally required to verify this information. Having it ready from the get-go prevents those frantic, last-minute searches for a misplaced document.

Analyze Your Credit and Debt

Your credit score is one of the single biggest factors in getting a mortgage. It directly impacts your interest rate and whether you get approved at all. Before you apply, pull your credit reports from all three main bureaus—Equifax, Experian, and TransUnion. You can get them for free once a year.

Look through each report with a fine-tooth comb. Seriously. A simple mistake, like a car loan you paid off still showing a balance, can drag your score down. If you spot anything wrong, dispute it immediately. Just know that the correction process can take a little while, so it’s best to do this early.

A strong credit score isn't just about getting a "yes" from the lender. It can literally save you tens of thousands of dollars over the life of your loan by securing a lower interest rate.

Next, it’s time to look at your debt-to-income (DTI) ratio. This sounds complicated, but it's simple math. Just add up all your monthly debt payments (car loans, credit cards, student loans) and divide that number by your gross monthly income. Most lenders want to see a DTI of 43% or lower. If yours is a bit high, focus on paying down some smaller credit card balances before you formally apply.

Set a Realistic Jenks Budget

Finally, you need a budget that reflects the real cost of owning a home here in Jenks. It's so much more than just the principal and interest on your mortgage.

You absolutely have to factor in property taxes, homeowners insurance, and any potential HOA fees. And don't forget maintenance! As a homeowner, you're on the hook for repairs. It’s also wise to have a basic understanding of Oklahoma building codes and what you need to know, because this can impact future costs for renovations or repairs.

Thinking about the full picture ensures you’ll be financially comfortable long after you get the keys to your new home.

What to Expect During Pre-Approval

Before you even think about looking at homes, getting pre-approved for a mortgage is the single most important thing you can do. It’s a game-changer. In a hot market like Jenks, a pre-approval letter from a trusted lender like Gateway Mortgage Jenks tells sellers you mean business.

This isn’t some back-of-the-napkin estimate. It’s a real, conditional commitment from Gateway to lend you a specific amount of money for your home purchase.

Think of it as your golden ticket for house hunting. You'll know exactly how much home you can realistically afford, which saves you the heartache of falling for a property that's just out of reach. It also gives your real estate agent serious leverage when it's time to negotiate.

How Your Financial Picture Is Evaluated

When you meet with a loan officer at Gateway, they’re going to take a deep dive into your finances. This is where all that paperwork you gathered comes into play. They’re looking at a few key things to figure out your borrowing power.

Your loan officer will be analyzing your income stability, credit history, and any existing debts. For example, a buyer with a five-year track record at their job, a solid 740 credit score, and minimal credit card debt is a strong candidate. On the other hand, someone newer to their career or carrying more debt might get approved for a smaller amount.

This detailed review is what makes a pre-approval so much more powerful than a simple pre-qualification, which is often just based on information you provide without verification.

Understanding Your Pre-Approval Amount

The number on your pre-approval letter isn't pulled out of thin air. It’s calculated using your debt-to-income (DTI) ratio and the lender’s specific guidelines. Your loan officer will walk you through exactly how they got to that number and what your estimated monthly payment will look like—including principal, interest, taxes, and insurance (PITI).

Don't hesitate to ask questions. Getting comfortable with the terms of your potential loan now is absolutely critical.

Pro Tip: Your pre-approval amount is a ceiling, not a target. I always advise clients to shop for homes below their maximum. This leaves you with a comfortable financial cushion for unexpected repairs, maintenance, and all the other costs of homeownership.

This is also a great time to lean on your lender's experience. Gateway Mortgage has seen it all, funding an incredible $10.1 billion in residential loans in 2021 alone, even when the market was tight. That kind of volume means they know how to handle just about any financial situation and can offer advice that’s genuinely helpful.

Once you have that pre-approval letter in hand, you can start the fun part with confidence. Knowing your budget lets you zero in on the right neighborhoods and start exploring all the great things to do in Jenks, Oklahoma, as you find the perfect place to call home.

From Finding a Home to Final Loan Approval

Alright, with that pre-approval letter in hand, you’re officially in the driver's seat. This is when the house hunt in Jenks gets real. Once you find the home and the seller says "yes" to your offer, you'll sign a purchase agreement. That single document is what kicks the entire mortgage process into high gear.

Your first move? Get that signed contract over to your loan officer at Gateway Mortgage Jenks immediately. This is the moment your application officially switches from a pre-approval to a live loan file, and that triggers the next critical phase: underwriting. This is where all the behind-the-scenes magic happens.

As you get ready to make an offer, it's also a great time to be understanding what earnest money means and how that "good faith" deposit protects both you and the seller. It's a key part of showing you're a serious buyer.

Meet Your Loan Team Processor and Underwriter

Once your file goes live, you'll be introduced to your loan processor. Think of the processor as your loan's project manager. Their job is to collect every last piece of necessary paperwork—from that purchase contract to your most recent pay stubs—and package it up perfectly for the underwriter.

They’ll be in touch frequently, so responding quickly is your best strategy.

The underwriter is the one who gives the final thumbs-up on your loan. They are meticulous, reviewing every single piece of your financial puzzle to make sure it lines up with Gateway's lending guidelines. They'll verify your income, assets, and credit one last time, and they'll also take a hard look at the property itself.

Key Insight: Don’t panic if the processor or underwriter asks for more information. It happens all the time and is a completely normal part of the process. A request for a specific bank statement or a letter explaining a recent deposit isn't a red flag; it's just the team doing their due diligence to get your loan across the finish line.

The Property Verification Phase

While your finances are getting a final look, Gateway is also kicking off the property evaluation. This isn't just about what you can afford; it’s about making sure the home is a solid investment for everyone involved—you and the bank.

This part of the journey has three core components:

The Appraisal: An independent appraiser will visit the Jenks property to figure out its fair market value. Lenders need to confirm the home is worth at least what you're borrowing.

The Title Search: A title company goes to work, digging through public records to check the property's history. They’re looking for any outstanding liens or ownership squabbles to ensure you receive a "clear title."

Homeowners Insurance: You’ll need to shop for and secure a homeowners insurance policy. Before your loan can be finalized, you have to provide proof of coverage to Gateway.

After your offer is accepted, the next few weeks are a whirlwind of activity. This table breaks down the key stages leading up to closing day.

Key Stages from Contract to Closing

Stage | Your Responsibility | Gateway's Responsibility | Estimated Timeframe |

|---|---|---|---|

Initial Submission | Send signed purchase contract to your loan officer. Provide earnest money deposit. | Order appraisal and title search. Assign processor. | 1-3 Days |

Processing | Respond promptly to all requests for updated documents (pay stubs, bank statements). | Gather and organize all documentation for the underwriter. | 1-2 Weeks |

Underwriting | Provide any additional explanations or documents the underwriter requests. | Review all financial and property details to ensure loan meets guidelines. | 1-2 Weeks |

Final Approval | Secure homeowners insurance. Review initial Closing Disclosure. | Issue a "Clear to Close" once all conditions are met. | 3-5 Days |

As you can see, it's a collaborative effort. Keeping the lines of communication open is the best way to ensure everything stays on track.

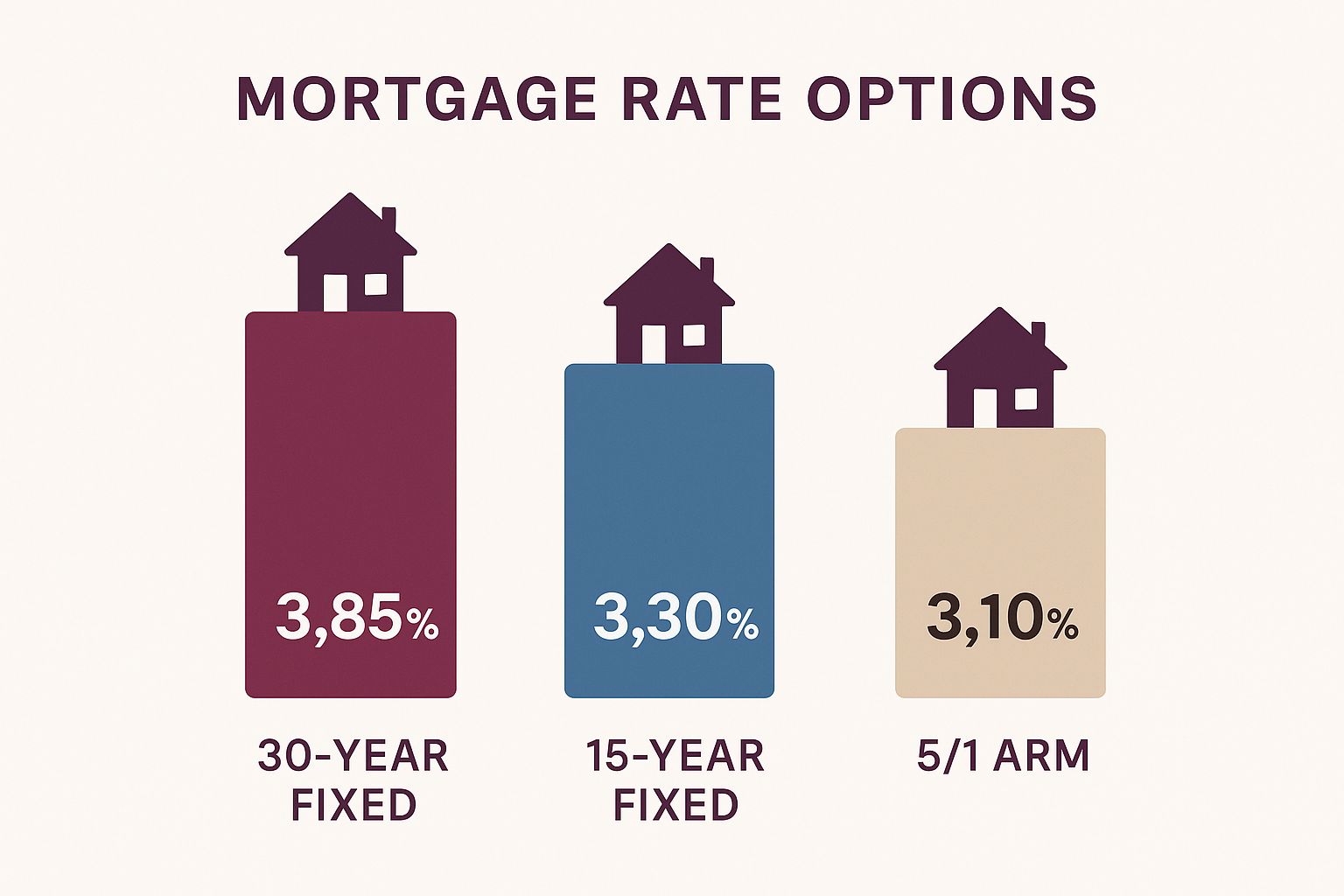

This visual helps compare some common mortgage rate options so you can see how different loan structures work.

It highlights how a shorter loan term, like a 15-year fixed mortgage, usually comes with a lower interest rate, which can help you build equity in your home much faster. This entire underwriting period typically takes a few weeks. The absolute best thing you can do to keep things moving is to respond quickly to any requests from your team at Gateway Mortgage Jenks. Prompt communication truly is the secret to a smooth and timely closing.

Navigating Your Closing Day with Confidence

You’re in the home stretch now. All the paperwork, the waiting, the anticipation—it all leads to this final step before you get the keys to your new place in Jenks. This is where everything comes together, and if you know what to expect, closing day is more of a celebration than a stress-fest.

The best phrase you can hear at this point is "Clear to Close." When your Gateway Mortgage loan officer gives you that call, it's the official green light. It means the underwriter has given the final sign-off on your loan, and you're ready to make it official.

Decoding Your Closing Disclosure

A few days before you sit down to sign, you’ll get a five-page document called the Closing Disclosure (CD). Think of it as the final, itemized receipt for your home loan. It’s absolutely critical that you review this thing with a fine-tooth comb.

Pull out the Loan Estimate you got at the very beginning of this journey and compare them side-by-side. The figures should line up pretty closely. Pay special attention to these key numbers:

Loan Amount: Is this the total you agreed to borrow?

Interest Rate: Does this match the final rate you locked in?

Closing Costs: Check the fees for the appraisal, title search, and other services.

Cash to Close: This is the big one—the exact dollar amount you need to have ready on closing day.

If something seems off or just doesn't make sense, don't hesitate. Call your loan officer at Gateway Mortgage Jenks immediately. It’s their job to walk you through it and make sure you’re 100% confident in the numbers before you sign.

Preparing for the Final Signature

Your closing will take place at a local title company, and you’ll need to bring a couple of important things to make sure it all goes smoothly.

Your cash to close is the most important piece of the puzzle. It has to be a cashier's check or a wire transfer—they won't accept a personal check for this final payment. Make sure you get this sorted out with your bank a day or two beforehand.

You'll also need a valid, government-issued photo ID, like a driver's license, for every person signing the loan documents. The signing itself usually takes about an hour. A closing agent will guide you through the stack of paperwork, explaining each document as you go.

This is where having a trusted local lender really pays off. Gateway Mortgage is headquartered right here in Jenks, and they know the local market inside and out. They funded over $11.3 billion in mortgage loans in 2020 alone, which tells you they have a ton of experience getting families to the finish line.

Once that last page is signed, the keys are yours. Congratulations! Of course, the work isn't quite over. For some great tips for a less stressful move, check out this helpful guide. And once you’re all settled in, you can start exploring your new community—our guide to the Oklahoma Aquarium right here in Jenks is the perfect spot for a first family outing.

Common Questions About Gateway Mortgage in Jenks

Stepping into the mortgage process always kicks up a few questions, and that’s especially true when you've got your eye on a specific lender and community. When it comes to landing a Gateway Mortgage in Jenks, I've found that most homebuyers run into the same handful of curiosities. Getting those answers squared away early on makes the whole experience feel less daunting.

I’ve put together some of the most common questions I hear to give you some quick, practical info. This is your go-to guide for understanding the nuts and bolts of working with a true hometown lender.

What Types of Home Loans Can I Get?

This is usually the first question people ask. The good news is Gateway Mortgage has a solid lineup of loan options, so you’re not stuck with a one-size-fits-all product. They really cover the bases for Jenks homebuyers.

Here’s a quick look at what they offer:

Conventional Loans: The go-to for borrowers with solid credit and at least a 3-5% down payment.

FHA Loans: Backed by the government, these are a fantastic option for first-time buyers. They come with lower down payment needs and more wiggle room on credit scores.

VA Loans: This is a huge perk for our veterans and active-duty military. These loans often require no down payment whatsoever.

USDA Loans: If you're looking at properties in the more rural or suburban parts of the area, a USDA loan might be a perfect fit.

Jumbo Loans: For those beautiful, higher-priced Jenks homes that go beyond the standard loan limits.

This spread means that whether you're just starting out or buying your forever home, there's a good chance Gateway has a loan that aligns with where you are financially.

How Long Does the Process Usually Take?

Everyone wants to know the timeline—when do I get the keys? While every loan has its own quirks, you can generally expect the process with Gateway Mortgage to take about 30 to 45 days from application to closing.

Of course, a few things can speed that up or slow it down. The appraisal, the title search, and how quickly you get your documents in all play a role. The secret to a smooth closing? Stay in close touch with your loan officer. Answering their emails and calls promptly can literally shave days off your timeline.

A proactive borrower is an on-time borrower. By having your documents organized and being ready to respond, you can often shave days off your closing timeline.

Is It Better to Use a Local Lender?

Absolutely. The advantage of using a local Jenks lender like Gateway is huge. Their loan officers don’t just have an office here; they live here. They know the Jenks real estate market inside and out—from neighborhood value trends to which real estate agents are the most responsive.

That kind of local knowledge is priceless. It often makes for a much smoother transaction because your lender, agent, and title company probably already know each other and have a system down. And beyond just the loan, homebuyers are choosing a community. If you're curious about the local vibe, you can learn more in our guide that looks into how safe the Jenks, Oklahoma area is for families.

Ultimately, choosing a lender with deep roots in Jenks gives you a real leg up. It can turn what feels like a stressful process into a more connected and supportive journey home.

Ready to explore the heart of your new community? The Ten District offers a vibrant mix of local shops, dining, and events right on Jenks Main Street. Discover what makes downtown Jenks special by visiting us at https://www.thetendistrict.com.

Comments